Nearly every student is eligible for some form of financial aid from the government, their college, or private organizations. This aid can come in the form of grants, scholarships, work-study programs, federal student loans - or 0% interest loans from JELF! Students who may not qualify for need-based aid, such as Pell Grants or subsidized federal loans, can still be eligible for unsubsidized federal loans regardless of their family income or financial circumstances.

Most importantly, be sure that you prepare effectively for college by making informed financial decisions early on. Explore JELF's resources for saving, budgeting, and understanding the costs of higher education. Access our helpful questionnaire to gauge your readiness and ensure you're on track with your college savings!

Understanding the True Cost of College

College expenses extend far beyond tuition. To effectively plan and budget, families must understand the full scope of costs associated with higher education.

Understanding and planning allows families to make informed decisions, manage their finances effectively, and reduce the financial burden of higher education. This approach ensures a clearer path to achieving educational goals without unexpected financial strain.

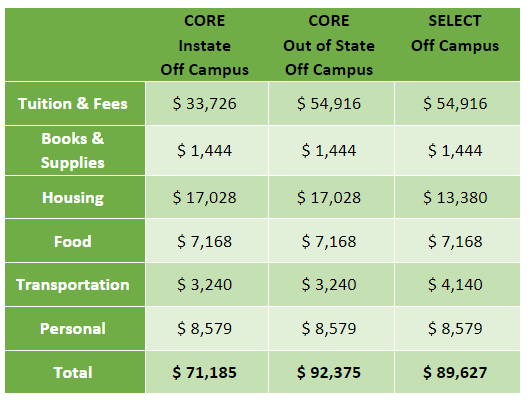

Understanding the costs associated with different types of colleges and their locations is crucial for effective financial planning. The following charts provide a detailed breakdown of tuition fees, advantages, and challenges for various college types, as well as the impact of location on living expenses and overall costs. This information can help students and families make informed decisions about higher education options.

Type of College

Tuition and Fees

Advantages

Challenges

Community Colleges

Lower tuition rates compared to four-year institutions. In-district and out-of-district rates available.

Affordable for general education. Flexible schedules for part-time work.

Limited resources and extracurriculars. Complex transfer process. Ensure credits transfer.

Four-Year Public Universities

In-State Colleges

Average annual tuition: $10,000 - $15,000

Lower cost for state residents. Access to state-sponsored scholarships and grants.

Limited spots due to high demand. High competition for state-specific scholarships.

Out-of-State Colleges

Average annual tuition: $25,000 - $35,000

Broader selection of programs and institutions. Opportunities for diverse experiences and networking.

Higher tuition and additional costs. Limited eligibility for state-specific financial aid.

Private Universities

Average annual tuition: $35,000 - $50,000+

Substantial financial aid packages. Smaller class sizes, personalized attention, extensive resources. Strong alumni networks.

High sticker price without financial aid. Intense competition for admission and scholarships.

Vocational Schools

Programs: a few thousand dollars to around $20,000

Shorter program durations. Hands-on training in specific trades. High job prospects and earning potential for skilled trades.

Limited scope of education. May require extra certification or licensing. More limited financial aid options.

Financial Aid Impact

Merit-Based Aid

Generous merit-based scholarships at private universities. Merit scholarships to attract top students.

Need-Based Aid

Substantial need-based financial aid at private institutions. Less flexibility for public universities.

Location Impact Chart

Location

Cost of Living

Advantages

Challenges

Urban Campuses

Higher living expenses. On-campus housing more expensive but convenient.

Access to internships, jobs, cultural events, public transportation. More networking opportunities and resources.

Higher overall costs due to living expenses. Potential for distraction.

Rural Campuses

Lower housing and living expenses. Affordable off-campus housing.

Lower overall cost of attendance. Close-knit community, less distraction from studies.

Fewer job and internship opportunities. Limited access to amenities and services.

Regional Differences

Northeast

High tuition and living costs. Higher cost of living in cities like Boston and New York City.

Home to prestigious private universities.

High cost of living and tuition.

Midwest

More affordable public universities and cost of living.

Strong state university systems with good value for in-state students.

South

Lower tuition and cost of living compared to Northeast and West Coast.

Growing number of reputable public and private institutions.

West Coast

Higher cost of living in cities like Los Angeles and San Francisco. High tuition for out-of-state students.

Many colleges offer online cost calculators that provide an estimate of tuition and fees, room and board, and other expenses based on specific student information. These tools can give you a realistic idea of the total cost of attendance, helping you plan more effectively. Take advantage of these calculators early in your planning process to set accurate financial expectations.

Creating a Detailed Budget

Break Down Estimated Costs into Categories: Divide your college expenses into clear categories such as tuition, housing, food, books, transportation, and personal expenses. This makes it easier to manage and monitor your spending.

Track All Expenses: Keep a detailed record of all expenses, both expected and unexpected. Use budgeting apps or spreadsheets to help you stay organized. Regularly compare your actual spending to your budget to ensure you stay on track.

Adjust as Necessary: Be prepared to adjust your budget as needed. College costs can change, and personal circumstances can vary, so flexibility is key. Regularly review your budget and make adjustments to address any discrepancies or changes in your financial situation.

Plan for Unexpected Costs by Setting Aside a Contingency Fund: It's important to have a contingency fund for unplanned expenses such as medical emergencies, car repairs, or sudden increases in living costs. Aim to set aside a small percentage of your budget to cover these unexpected costs, providing a financial safety net.

Utilizing Financial Aid and Scholarships

Maximize Financial Aid: Complete the Free Application for Federal Student Aid (FAFSA) as early as possible to determine your eligibility for federal grants, loans, and work-study programs. Stay informed about deadlines and required documents to ensure you don't miss out on available aid.

Apply for Scholarships: Continuously search and apply for scholarships throughout the year. Many scholarships have specific criteria and deadlines, so it's important to stay organized and keep track of applications. Scholarships can significantly reduce the overall cost of college.

Managing Day-to-Day Expenses

Limit Discretionary Spending: Be mindful of non-essential expenses such as dining out, entertainment, and shopping. Finding affordable alternatives and sticking to your budget can help stretch your funds further.

Take Advantage of Student Discounts: Many businesses offer discounts to students with a valid student ID. Take advantage of these discounts for purchases such as software, transportation, and dining.

Work Part-Time: Consider finding a part-time job or work-study position to earn extra income. Working while in school can help cover day-to-day expenses and reduce the amount you need to borrow in student loans.

By following these budgeting strategies, you can effectively manage your college expenses and reduce financial stress, ensuring you can focus on your academic and personal growth.

Living On-Campus: On-campus housing can often be more convenient and sometimes more cost-effective than off-campus options. It typically includes utilities and other amenities, and you may save on transportation costs by living close to classes and campus facilities.

Off-Campus Housing Options: Look for less expensive off-campus housing alternatives. Consider sharing an apartment or house with one or more roommates to significantly reduce rent and utility expenses. Additionally, becoming a resident assistant (RA) can offer substantial savings on room and board costs, sometimes even covering them entirely.

Campus Dining Plans: Take full advantage of campus dining plans to avoid unnecessary food expenses. Use meal swipes and dining dollars wisely, and plan your meals to minimize additional grocery or dining-out costs. Look for discounts or promotions offered by campus dining services, and consider opting for meal plans that best suit your schedule and eating habits to avoid wasting unused swipes or funds.

Textbooks and Supplies

Buy used or digital textbooks, or utilize library resources when possible.

Sell textbooks back or participate in book swaps at the end of each semester.

Many retailers and service providers offer discounts for students. Always ask and take advantage of these opportunities. Here is a list of just some of the types of student discounts that often exist.

Technology and Software

Discounts on laptops, software, and accessories from major tech companies.

Free or discounted access to popular creative and productivity software.

Streaming Services

Reduced rates on music, video, and other entertainment streaming services.

Transportation

Discounts on public transit, train, and bus fares.

Reduced membership rates for car-sharing services.

Clothing and Retail

Discounts on fashion, athletic wear, and accessories from various retailers.

Food and Dining

Discounts available at some fast-food chains and local restaurants near campuses.

Insurance

Affordable student health insurance plans through colleges.

Good student discounts on car insurance from major providers.

Entertainment

Reduced admission prices at movie theaters, museums, and zoos.

Discounts on tickets for concerts, sports events, and other entertainment.

Travel

Discounted flights, accommodations, and travel packages for students.

International student discount cards for various services and experiences.

Books and Supplies

Discounts on textbooks, school supplies, and rentals from major bookstores and online retailers.

Financial Services

No monthly fees on student bank accounts.

Student-focused credit cards with rewards and no annual fees.

Fitness and Wellness

Reduced rates for gym memberships and fitness classes.

Tips for Maximizing Student Discounts

Always Ask: Inquire about discounts when shopping or dining.

Carry Your Student ID: Keep it handy for verification.

Utilize Student Email: Sign up using your .edu email address.

Stay Informed: Use websites/apps that list student discounts.

By taking advantage of these general categories of student discounts, students can save money and make their college experience more affordable.

Financial Aid Tools for Today's Students

To better understand all the different types of financial aid available, you visit the website for the FAFSA. This is the official U.S. government website for federal student aid, and it provides comprehensive information on grants, scholarships, work-study, and federal student loans.

The key is to explore all the different financial aid options, as there are many opportunities for students to get help paying for their education, even if they don't initially qualify for need-based aid. Thoroughly researching the available resources can make a significant difference in a student's ability to afford college.

The FAFSA (Free Application for Federal Student Aid) is a form that can be prepared annually by current and prospective college students in the U.S. to determine eligibility for student financial aid.

Once you submit the FAFSA (which is something you'll need to do EVERY year of school), you’ll receive your FAFSA Submission Summary, which details the information you included on the application and your SAI. (This summary was previously called the Student Aid Report.)

It is important to realize that though FAFSA is the application for financial aid, once you learn what financial aid you will be receiving, the financial aid itself actually comes from your school or university.

These are the main criteria for FAFSA, but for complete list, visit FAFSA.

U.S. citizen, U.S. national, or eligible non-citizen

Valid Social Security number

Enrolled or accepted as a regular student in an eligible degree or certificate program

Maintains satisfactory academic standing

Has a high school diploma or GED

Signs the certification statement stating that:

They are not in default on a federal student loan and do not owe money on a federal student grant and

Federal student aid will only be used for educational purposes.

Students mustsubmit the FAFSA each year they are in school to get all eligible federal student loans, grants, work-study and even some private scholarships.

In the 2024-2025 academic year, the Student Aid Index (SAI) replaced Expected Family Contribution (EFC).

The information you input on the FAFSA about you and your family’s financial profile will determine your SAI. The index will equal the sum of your parents’ available income, your income and assets.

Unlike the old EFC, the SAI will not consider the number of family members in college. This means that parents will no longer receive a sibling discount.

The Federal Direct Loan Program (subsidized or unsubsidized), formerly known as the Stafford Loan, is the most standard type of long-term, fixed rate student loans.

An unsubsidized federal student loan is a type of student loan offered by the federal government where interest begins to accrue from the time the loan is disbursed, regardless of whether the student is still in school or during any deferment periods. Unlike subsidized loans, the borrower is responsible for paying all the accrued interest, which can be paid while in school or added to the principal amount of the loan, increasing the total amount to be repaid. These loans are available to both undergraduate and graduate students, and financial need is not a requirement for eligibility, though students can choose to defer the payments until after graduation.

No matter what a student's need is, all students receive the same amount from the Federal Direct Loan Program based on what year of school or program they are in:

Undergraduate Students:

Freshman: $5,500

Sophomores: $6,500

Juniors / Seniors: $7,500

Most undergraduates receive a portion of their Federal Direct Loan as subsidized and a portion unsubsidized. However, this depends on demonstrated financial need.

Graduate Students:

$20,500 / year (with exceptions for law and medical schools).

Since July 2012, graduate and professional students have not been eligible to receive subsidized loans.

A federal loan is a broad term for any student government loan that is typically a low-cost (or no cost), fixed-rate loan available to undergraduate students, graduate students, and parents of dependent undergraduate students. There are many different types of federal loan programs:

ACG (Academic Competitiveness Grant) – This is a federal grant that may be awarded only to 1st and 2nd year Pell Grant (see below) recipients who have completed specific rigorous high school curricula. Funding is limited, so not all students receive this grant.

College Work-Study Program – This is a federal program which provides jobs for students who must earn part of their educational expenses. Funds are provided by the government to the school, and an on-campus job is assigned by the school. The amount varies and does not need to be repaid.

Direct PLUS Loans – These are federal loans that graduate or professional students and parents of dependent undergraduate students can use to help pay for college or career school. There is a loan fee on all Direct PLUS Loans. Interest rates for Direct PLUS Loans = 6.31%. However, if you got your Direct PLUS Loan on or after July 1, 2022, and before July 1, 2023, the loan will have a fixed interest rate of 7.54% after the payment pause ends.

Graduate PLUS Loan - This is a non need-based student loan which allows graduate or professional students enrolled at least half time at an eligible school in a program leading to a graduate or professional degree or certificate to borrow up to the total cost of graduate education (determined by the school) minus other aid. These loans can be deferred while the student is in school and, if credit is sufficient, a cosigner is generally not needed.

Parent PLUS Loan – This is a federal loan offered to parents of dependent, undergraduate students who are enrolled at least half time at participating and eligible post-secondary institutions. Good credit, not financial need, is required.

To receive a Parent PLUS Loan, the parent(s) must not have an adverse credit history. Parents may borrow up to the total cost of the student attending college (determined by the school) minus any other financial assistance received. Repayment begins 60 days after funds are disbursed but may be deferred for a 6-month period after the student graduates. If a parent borrower is unable to obtain a PLUS loan, the undergraduate dependent student may be eligible for additional unsubsidized loans.

National SMART Grant – Federal SMART grants may be awarded to 3rd and 4th year Pell recipients who are enrolled in specific math or science majors. Similar to the ACG, funding is limited, so not all Pell recipients receive these.

Pell Grant – This is a need-based grant which is awarded to students with the highest calculated financial need and does not have to be repaid. The maximum Pell Grant is currently $7,395 per year. Eligibility is based on a financial formula. These grants are limited to students with financial need who have not earned their first bachelor’s degree.

SEOG (Supplemental Educational Opportunity Grant) – Federal loan awarded to Pell Grant recipients who have the highest need. Schools receive a limited amount of SEOG from the federal government, so not all Pell recipients will receive it. Amounts range from $100 to $4,000. The SEOG does not have to be repaid.

A subsidized Federal Direct Loan means that the government will subsidize the interest while the student is enrolled or in deferment. This loan is awarded on the basis of financial need. Approximately 2/3 of subsidized Federal Direct loans are awarded to students with family gross incomes under $50,000.

Unsubsidized Federal Direct Loans

An unsubsidized loan means that the student is responsible for paying the interest on the loan from the minute the loan is granted. Students may, however, have payments deferred until after graduation, at which point they may take 10-25 years to repay. This loan is not awarded based on need, which means that all students are eligible for it. The interest that accrues is capitalized and added to the principal.

Graduate students are automatically considered “independent” of their parents for purposes of obtaining federal loans and completing the FAFSA, regardless of their age. This means that their eligibility for federal aid is determined based on their own financial situation, not their parents'. However, the FAFSA still recommends that medical students fill out the parent sections because individual medical schools may consider parental information when administering their own financial aid packages.

The reasoning behind this recommendation is that some medical schools use parental information to assess the financial background of their students. If a student comes from a low-income family, the school might offer more generous institutional aid to help offset the costs of medical education. This can include grants, scholarships, or other forms of financial assistance that do not need to be repaid. By providing parental financial information, students can potentially increase their eligibility for this additional aid, which can significantly reduce their reliance on loans and lower their overall debt burden after graduation.

Essential Documents for Your Financial Aid Application

Applying for financial aid can feel overwhelming, but having the right documents ready will streamline the application process and increase your chances of receiving the maximum amount of aid possible. To ensure you submit a complete financial aid application, use these tools below to learn about the essential forms and records you may need to provide.

Remember, the specific documents required may vary depending on your personal circumstances and the type of aid you are seeking, so be sure to check with your school's financial aid office for any additional guidance.

These documents encompass the most common items required for federal, state, and institutional financial aid applications. Depending on your unique situation, you may need to provide some or all of these materials. Take the time to carefully review each item and have them readily available when you begin filling out your financial aid forms.

If you have any questions or need assistance gathering these materials, be sure to reach out to your college's financial aid department for support.

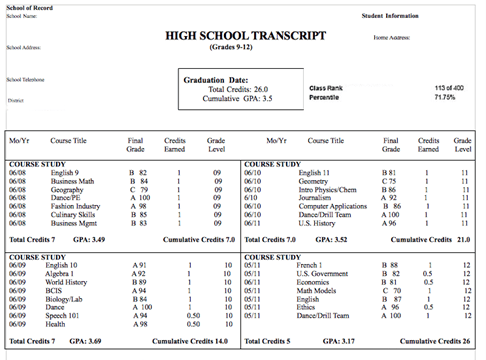

Financial aid applications often require a student's unofficial transcript (i.e. grades) through their most recently completed semester of school. This must include the student's cumulative GPA. Students typically do not need to pay for an 'official' transcript; a screenshot is fine (see below).

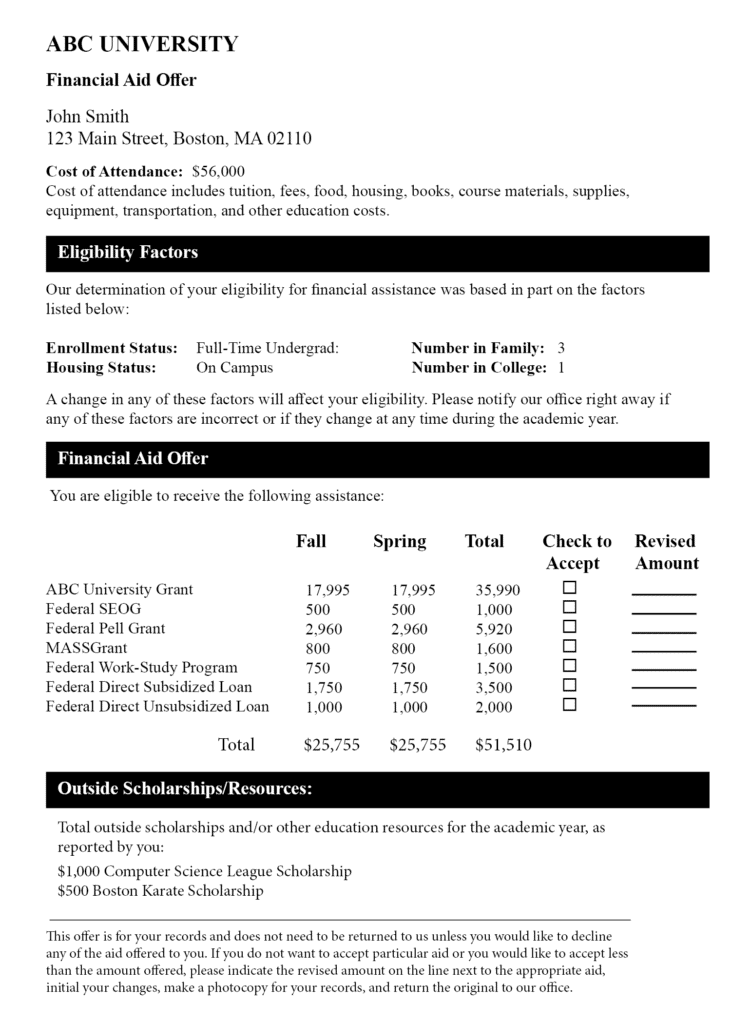

Students will find their Financial Aid Award in their school's student portal. It is important to ensure that this is the award for the academic year in which they are applying for a loan, not a previous year's award.

While each school’s award summary will look different, students will typically need the financial aid award that has been ACCEPTED, not just the award letter showing what the student has been offered.

These are the total federal loan amounts that students are offered for each academic year:

Level

Amount

Freshman

$5,500

Sophomore

$6,500

Junior

$7,500

Senior

$7,500

Second Bachelor’s Degree

$12,500

Graduate Student

Min. $20,500

Each school’s award summary will look a little bit different. Here is a sample:

A school's cost of attendance can be found in a student account, the school’s website or within the student's financial aid letter. This document should show the expected breakdown of costs such as tuition, dorm & board, fees, etc. If there are additional costs related to a student's program, students should explain this, including the amount and what the amount covers, wherever possible.

The FAFSA Submission Summary (previously known as the Student Aid Report or SAR) summarizes the information a student submitted on their FAFSA and provides information about financial aid eligibility based on that information.

After a student's FAFSA form is submitted and processed, they will receive an email from FAFSA with instructions on how to access an online copy of their FAFSA Submission Summary. This will include the estimated eligibility for federal student loans, a Federal Pell Grant (if student qualifies for one), the Student Aid Index (SAI) and whether the student has been selected for verification. Being selected for verification happens at random and does not mean that a student has done anything wrong. Students will need to provide the documentation that is requested of them by a specific deadline to ensure that they can still get federal student aid.

Once a student's FAFSA form has been processed, they can get a copy of their FAFSA Submission Summary by logging in to FAFSA using their account username and password, navigating to your account Dashboard, selecting your processed FAFSA submission, and then selecting the “View FAFSA Submission Summary.”

Students will need to upload an image of their driver's license, state ID or passport. The image uploaded must include a photo of the student.

Examples:

Scholarships and More

In addition to our student loan offerings for Jewish students, JELF also provides a list of scholarships and other financial aid options that all students can access. This comprehensive resource can help you identify and apply for additional funding opportunities to support your educational goals.

Whether you are in a preschool stage -- or already in high school -- JELF's roadmap will help you navigate the financial aspects of college planning with confidence and ease.

JELF Application FAQ

JELF (Jewish Educational Loan Fund) is a non-profit organization that provides interest-free loans to Jewish students in need. JELF's mission is to enable Jewish students to access educational opportunities that may otherwise be out of reach due to financial constraints.

JELF loans can be used for a variety of educational expenses, including tuition, room and board, textbooks, and other approved costs. Students can apply for JELF loans for undergraduate, graduate, and professional degree programs. The application process is straightforward, and eligible students are encouraged to apply during the regular financial aid cycle for their educational institution.

JELF takes both the total cost of the student’s education as well as the family’s total resources into account. Defining need is both personal as well as different for different families. Need is based not only on household income but also the number of individuals in a household, as well as a medley of other factors related to health or employment that may directly alter what funds exist for a student’s higher education.

Learn more here about JELF’s process for determining each applicant’s loan amount.

JELF loans are based on financial need, not a student’s GPA. In order to be eligible (or stay eligible) for funding, all loan recipients must prove to be in good academic standing each semester.

JELF loans are available for students attending U.S.-accredited universities, vocational, or CTE (Career & Technical Education) programs. If a school is eligible for FAFSA, it meets JELF’s criteria.

Although most international universities are not FAFSA-eligible, JELF has funded programs outside the U.S., such as the American Medical Program at Tel Aviv University in Israel, which is accredited through NYU.

To determine if an international school qualifies for FAFSA, please contact the university or program directly.

Because JELF provides “last dollar” funding—filling in the final gap after all other financial aid has been applied—students are required to accept all federal Direct Subsidized and Unsubsidized Loans that are offered to them. These loans typically carry the lowest interest rates and most flexible repayment terms, and accepting them is a requirement before JELF can step in to help. However, JELF does not require families to take out Parent PLUS, Grad PLUS or any other high-interest private loans.

Yes! Thanks to the Judith and Aaron Alembik Endowment, JELF has established a dedicated fund specifically to support the children of Jewish clergy. This endowment ensures that eligible clergy children have access to JELF’s interest-free loans as part of the regular application process, helping them pursue higher education without the burden of high-interest debt.

This fund is not intended for students who are studying to become rabbis, cantors, or other Jewish clergy themselves. Rather, it is intended to assist the children of clergy in financing their undergraduate or graduate education. To learn more about this unique opportunity and eligibility requirements, visit jelf.org/clergy.

No. Each year JELF receives more applications than we can fund. JELF’s Loan Review Committee carefully evaluates every applicant’s financial and personal circumstances, and awards are made based on relative need. If a student is not funded this year, they are welcome to apply again in the future.